Blog

Insights, Trends & Market News

Financial health is an extremely important factor in achieving financial success and stability over the long term. Unfortunately, far too many people make mistakes that can have a lasting and serious impact on their overall financial well-being. Read the following 5 common financial mistakes I see in order to mitigate your risk while keeping your financial plan strong and successful.

1. Trying to “Beat the Market”

We all invest with the hope that one day we won’t have to work and will have enough money to live off our investments. Many people wonder: Can a regular investor really beat the market? While some of us have the tools and connections required to make knowledgeable decisions that could lead to a portfolio with higher returns, it’s others, like stockbrokers, bankers, and big corporations, that likely have the advantage. This is because they possess the necessary financial statement analysis skills to develop a greater insight about a given company. The truth is, the average individual investor has little chance of beating the market. A trusted financial partner can provide knowledge to help you make financial decisions that don’t risk harm to your portfolio.

2. Not Planning for Unexpected Risks

Very few people, if any, predicted COVID-19 or the Great Recession. But these two events have made it abundantly clear that unexpected economic downturns must be considered when building a comprehensive wealth management strategy. People often think that an emergency fund is enough to ride out unforeseen major life events, but it usually takes more than that. At Rosemeyer Management Group, we believe that proper risk management is key to staying afloat during uncertain times. This can be accomplished by considering unexpected risks that are personal in nature, such as divorce, disability, accidents, and illness, and by making sure you are properly covered.

3. Not Understanding Diversification

When it comes to investing, asset allocation is the equivalent of deciding how many of your eggs you’re going to put into how many different baskets—or asset classes. Diversification is the spreading of your investments both among and within different asset classes. Your asset allocation will depend on a number of factors, including your risk tolerance and investment horizon. Diversifying your portfolio can reduce the risk of major losses that may result from over-emphasizing a single asset class. Stocks and bonds, for instance, often move in different directions from each other, which is why holding both of these asset classes (and others) can help manage risk. By understanding the role different asset classes play in your portfolio, you can increase the probability that some of your investments will provide satisfactory returns, even if others are flat or losing value.

4. Paying More in Taxes Than Necessary

Of course, we all need to do our civic duty and pay our dues to Uncle Sam. But it’s important to know that there are ways to reduce some—or all—of your tax bill legally. The IRS offers Americans a variety of tax credits and deductions that can legally reduce how much you’ll owe. If you want to save money, consulting with a financial professional or tax advisor can help you create an efficient tax strategy while reducing your tax bill without getting in trouble for tax fraud. It’s important to know what deductions and credits you may be eligible for; and not knowing may result in you leaving money on the table.

5. Not Reaching Out for Help

Let us be the first to commend you for taking the time to learn and understand how to avoid costly mistakes in your financial plan. At Rosemeyer Management Group, we understand that it can be difficult to find the time to stay up to date on the many options for managing your finances. That’s why we offer a personalized financial plan that takes into account your individual values, goals, money mindset, and risk tolerance. We aim to keep you in the driver’s seat of your finances and support you in making changes as you see fit.

To get started, take advantage of our free introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to reach out to me at payton@rosemeyermg.com. We look forward to helping you find greater financial success!

About Payton

Payton Simon is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Payton spends his days providing in-depth investment analysis and aiding in the development of customized, comprehensive retirement, tax, and estate planning strategies to help his clients reach their retirement goals. Payton is passionate about doing his best for every client he serves and making sure they don’t have any blind spots or missed opportunities in their financial plan. He strives to do his part to close the financial literacy gap so people can feel confident and empowered about their financial future. Payton has a bachelor’s degree in finance with a minor in accounting from the University of Wisconsin-LaCrosse. Outside of work, Payton is active in his local Catholic parish and incorporates his faith into every aspect of his life. He loves spending time with his family and friends and is a sports enthusiast, playing golf, basketball, and baseball. To learn more about Payton, connect with him on LinkedIn.

Tax planning doesn’t have to be a tedious task! Taking a proactive approach to your taxes can actually save you time and money. At Rosemeyer Management Group, we help clients keep more of what they earn by minimizing their tax liability and maximizing their savings. Get the most out of your savings by reading our top 9 tax-planning strategies for 2023:

Maximize Your Retirement Contributions

Maximizing your retirement contributions is one of the best ways to minimize your tax liability. This is because retirement plans offer useful tax advantages that are not available if you were to simply put your money in a savings account. There are several accounts to consider, depending on your unique circumstances:

- 401(k), 403(b), and 457 Plans: These accounts allow you to contribute up to $20,500 annually for 2022 ($27,000 if over age 50). In 2023, these amounts have increased to $22,500 and $30,000 if over the age of 50. Not only that, but contributions are pre-tax so they won’t show up as part of your annual income. This is a great way to defer taxes until your retirement years when you could potentially be in a lower tax bracket.

- Roth 401(k) Plans: Many employers offer Roth contributions within their 401(k) plans. Similar to Roth IRAs, money is contributed on an after-tax basis, which means you cannot claim a current-year tax deduction. The upside is that your funds are left to grow tax-free for life. Usually Roth 401(k) plans are subject to the RMD requirement at age 72 (or 73 as of 2023), but the SECURE 2.0 Act has removed this requirement starting in 2024.

- Roth IRA: This is an attractive savings vehicle for many reasons, including no required minimum distributions (RMDs), tax-free withdrawals after age 59½, and the ability to pass wealth tax-free to your heirs. The contribution limits are the same as traditional IRAs. However, Roth IRAs have income restrictions and you may not be able to open an account outright if you are above certain limits.

- Traditional IRA: Contributing to a traditional IRA is another way to reduce your tax liability if your income is within certain limits. You can contribute up to $6,000 for 2022 and $6,500 in 2023. Both years have the same $1,000 catch-up contribution limit for those over age 50. Unlike the qualified retirement plans listed above, contributions to a traditional IRA can be made until the April 15th tax filing deadline.

Consider Roth Conversions

If you are outside of the income eligibility threshold for Roth IRAs but still want to take advantage of the Roth tax benefits, a Roth conversion could be the right strategy for you. It works by paying the income tax on your pre-tax traditional IRA and converting the funds to a Roth IRA.

Not only does this help you avoid the income threshold, but it is also a useful strategy during down markets. The value of your accounts will be lower, effectively allowing you to convert the account for a lower tax price. Once the market rebounds, you will have already converted your pre-tax funds to after-tax funds and all of your future earnings will be tax-free.

You could also consider the mega backdoor Roth and backdoor Roth IRA strategies:

- Mega Backdoor Roth: With this strategy, you would convert a portion of your 401(k) plan to a Roth. This involves first maximizing the after-tax, non-Roth contributions ($40,500 for 2022 and $44,500 in 2023) in your plan, then rolling it over to either a Roth 401(k) or your Roth IRA. With the mega backdoor Roth, you convert a portion of your 401(k) plan to Roth dollars.

- Backdoor Roth IRA: In this case, you would make an after-tax (non-deductible) contribution to a traditional IRA. You then immediately convert the funds to a Roth IRA to prevent any earnings from accumulating. This strategy makes sense if you don’t already have an IRA set up yet.

All three Roth conversion strategies will allow the contributions to grow completely tax-free and allow you to avoid future RMDs, which is helpful if you expect to be in a higher tax bracket in the future.

Contribute to a Health Savings Account

One of the most underutilized but most efficient ways to maximize your savings and minimize your taxes is to contribute to a health savings account (HSA). HSAs offer triple tax savings: contributions are tax-deductible, earnings grow tax-free, and you can withdraw the funds tax-free to pay for medical expenses. Unused funds roll over each year and will essentially become an IRA at age 65, at which point you can withdraw funds penalty-free for non-medical expenses. You must be enrolled in a high-deductible health plan in order to qualify for an HSA.

HSAs can be a great tax-management tool if you are able to pay medical expenses out of pocket and leave the HSA funds to grow. The 2022 contribution limits for HSAs are $3,650 for individuals and $7,300 for families. In 2023, the contribution limits jumped to $3,850 for individuals and $7,750 for families. If you are 55 or older, you may also be able to make catch-up contributions of $1,000 per year. You have until April 15th for your contributions to count for the previous year’s tax return.

Though the ultimate goal with an HSA is to keep the money growing for as long as possible, it’s important to keep your medical receipts in case you need to reimburse yourself in the future. The great part about HSAs is that you can reimburse yourself for expenses at any time as long as they were paid after your HSA was opened and you have the receipts to verify the amount!

Utilize Tax-Loss Harvesting

Tax-loss harvesting involves selling investments at a loss in order to offset the gains in your portfolio. By realizing a capital loss, you are able to counterbalance the taxes owed on capital gains. The investments that are sold are usually replaced with similar securities in order to maintain the desired asset allocation and expected return.

With the extreme market volatility of 2022, chances are you have some capital losses that can be utilized. For example, if you are expecting a large capital gain this year, sell an underperforming stock and harvest the losses to offset your gain.

Tax-loss harvesting can also be used to reduce your ordinary income tax liability if capital losses exceed capital gains. In this case, up to $3,000 can be deducted from your income, and capital losses in excess of this amount can be carried forward to later tax years.

Understand Long-Term vs. Short-Term Capital Gains

Understanding the tax implications of long-term versus short-term capital gains can go a long way in reducing your tax liability. For instance, in 2022 a married taxpayer will pay 0% capital gains tax on their long-term capital gains if their taxable income falls below $83,350. That rate jumps to 15% and 20% for taxable incomes that exceed $83,350 and $517,200, respectively. The thresholds increased slightly in 2023, but understanding where you fall on the tax table is an important part of minimizing your liability.

Gains that are short term in nature (held less than one year) will be taxed at your marginal tax bracket, which could be up to 37%! Knowing both the nature of your gain, as well as your tax bracket, is crucial information if you want to minimize your tax liability.

Contribute to a Donor-Advised Fund

If you itemize your tax deductions because of charitable contributions, you may want to consider investing in a donor-advised fund (DAF). You can contribute a lump sum all at once and then distribute those funds to various charities over several years. With this strategy, you can itemize deductions when you make the initial contribution and then take the standard deduction in the following years, allowing you to make the most out of your donation tax-wise.

You can also donate appreciated stock, which can further maximize your tax savings. By donating the appreciated position, you avoid paying the capital gain tax that would have been due upon sale of the stock and you are effectively donating more to your charities of choice than if you had sold the stock and donated the proceeds.

Make a Qualified Charitable Donation

If you own a qualified retirement account and are at least 70½, you can use a qualified charitable distribution (QCD) to receive a tax benefit for your charitable giving, and since this is an above-the-line deduction, it can be used in conjunction with other charitable tax strategies. A QCD is a distribution made from your retirement account directly to your charity of choice. It can also count toward your RMD when you turn age 72, but unlike RMDs, it won’t count toward your taxable income. Individuals can donate up to $100,000 in QCDs per year, which means a married couple can contribute a combined amount of $200,000!

Consider Estate Tax-Planning Techniques

Estate tax-planning techniques can also be an effective way to reduce current-year tax liability. For 2022, the lifetime exemption is $12.06 million for individuals and $24.12 for married couples; these amounts increase to $12.92 million and $25.84 million in 2023.

The annual gift tax exclusion has also been increased to $17,000 per recipient in 2023, up from $16,000 in 2022. This means that taxpayers can give this amount tax-free without using any of the previously mentioned lifetime exemptions. Not only that, but the annual exclusion applies on a per person basis, so each taxpayer can give $16,000 ($17,000 in 2023) per person to any number of people per year.

Though gifting and other estate tax-planning strategies are not tax-deductible, they can help to significantly reduce your taxable estate over time.

Make Sure Your Advisory Team Is Working Together

Beyond consulting with a tax professional, you’ll want to be sure your entire financial team is working together to provide cohesive oversight and guidance. This should include professionals like CPAs, financial advisors, investment advisors, and estate attorneys. Your finances don’t exist in a bubble and so neither will your tax-minimization strategies. When your advisory team works together, strategies are easier to identify and execute, and proactive tax solutions become much easier to implement, reducing stress and your tax bill.

Today Is the Day to Start Saving

Rosemeyer Management Group is here to simplify your tax-planning process. Our team of experienced advisors can help you minimize your tax burden and increase your savings. Plus, we provide a variety of tax strategies to suit your needs. To get started, schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to reach out to me at kaley@rosemeyermg.com. We look forward to helping you make the most of your finances.

About Kaley

Kaley Bockhop is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Kaley’s experience in taxes and accounting and her financial planning expertise allows her to help her clients work toward their retirement goals and set themselves up for success. It is Kaley’s goal to partner with her clients to build a customized road map for their finances so they can look forward to a comfortable retirement and decrease financial worry. Kaley is a CPA and a CERTIFIED FINANCIAL PLANNER™ professional. She has a bachelor’s degree in science from the University of Wisconsin-Platteville with a triple major in accounting, agricultural business, and animal science, and a minor in biology. In her free time, Kaley enjoys working on her family’s farm where they raise nationally recognized registered Angus show cattle. She also loves exercising and traveling. To learn more about Kaley, connect with her on LinkedIn.

Many of us share a similar worry: will we have enough money to last through all of retirement? But with a few tweaks, a few strategies, and the ability to lean on your financial advisor, you can create a plan that you’ll feel confident will take you all the way. Check out these three tips to help your retirement savings outlive you, not the other way around.

1. Identify Flexible Spending Categories

As you build your budget, organize it based on needs. Every single expense should be identified as either fixed or variable and essential or non-essential. For example, your housing expenses are likely fixed and essential. Food is essential, but it is a variable expense. A gym or country club membership may be fixed, but it is non-essential. Other forms of leisure or travel are likely variable and non-essential.

Knowing which expenses are necessary and which are flexible can relieve some of your concerns going into retirement. If you’re used to spending $8,000 a month, once you sort your expenses and discover that only $4,500 of them are truly necessary, it relieves a lot of pressure.

Identifying these spending categories also allows you to make wiser financial decisions and adjust better to market conditions. If we enter a bear market and your portfolio is down, you can cut spending back to cover the necessary expenses you identified. Maybe you put off that big trip or eat out less. This can potentially keep more of your money invested so you can be better positioned if and when the market bounces back.

2. Plan for Taxes

Unless all your money is in an after-tax account or Roth IRA, you’ll have to deal with taxes in retirement. Having your mortgage paid off before retirement is a common—and excellent—goal. However, don’t make the false assumption that no mortgage equals no payments.

Part of your monthly mortgage payment may be going toward property taxes and homeowners insurance if you escrow. Don’t forget that you still have to pay these bills when your home is fully paid off, and these figures must be included in your budget (and remember that these numbers will be inflating over time as well). One way to handle property taxes and homeowners insurance in retirement is to set aside money every month, just like you did with your mortgage. This way, you will have the funds available when those bills are due.

Property taxes won’t be the only taxes you’ll owe in retirement. Distributions from 401(k)s and IRA accounts will most likely be considered taxable income. Even your Social Security benefits may be taxable, depending on your overall income. It’s critical that you withhold and pay the proper taxes so you don’t get into a large tax bill situation. A competent tax preparer can help with this.

3. Work With a Professional

However, it’s not enough to only work with a tax preparer during retirement. Be sure to also work with a competent financial planner—it can mean the difference between a retirement marked by fear and stress and one of confidence.

Yes, it’s wise to have a financial professional help you with your investments during this next stage of life—but don’t stop there. You need your professional to help manage not only your money, but also your entire financial life.

At Rosemeyer Management Group, we understand the concerns people face as they plan for retirement. Not only do we answer your questions, we address the questions you haven’t thought to ask. To learn more, schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to reach out to me at payton@rosemeyermg.com.

About Payton

Payton Simon is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Payton spends his days providing in-depth investment analysis and aiding in the development of customized, comprehensive retirement, tax, and estate planning strategies to help his clients reach their retirement goals. Payton is passionate about doing his best for every client he serves and making sure they don’t have any blind spots or missed opportunities in their financial plan. He strives to do his part to close the financial literacy gap so people can feel confident and empowered about their financial future. Payton has a bachelor’s degree in finance with a minor in accounting from the University of Wisconsin-LaCrosse. Outside of work, Payton is active in his local Catholic parish and incorporates his faith into every aspect of his life. He loves spending time with his family and friends and is a sports enthusiast, playing golf, basketball, and baseball. To learn more about Payton, connect with him on LinkedIn.

If there’s ever a time when we need to stop and take stock of all we have to be grateful for, it’s now. With the dramatic events of the last two years, many of us were hoping that 2022 would be a fresh start. But even after a tough year in the markets, there is still so much to be thankful for. Our team is focusing on using this Thanksgiving season to cultivate a heart of gratitude and acknowledge the many things that enrich our lives on a daily basis.

Health

Gandhi said, “It is health that is real wealth and not pieces of gold and silver.” How true this is! We have seen time and time again over the years how health is the ultimate form of wealth—no matter how big or small the bank account. Our team members are thankful for the health they and their families have, and we hope you can join in our thankfulness on behalf of your loved ones.

Family & Friends

Speaking of loved ones, these are the people we are grateful to share important moments with and do life with day in and day out. But in this season especially, we are reminded of how much family means and the importance of surrounding yourself with people who know you, love you, and support you.

No matter how busy we are or what life changes come our way, family and friends are vital to our well-being. At Rosemeyer Management Group, we are incredibly grateful for the community that surrounds us, and we are privileged to consider many of our clients to be friends as well.

Freedom

This year brought shocking geopolitical events with the Russian invasion of Ukraine. Now, more than ever, we are reminded how privileged and blessed we are to live in a prosperous and free country. There are many people all over the world who long to live here, and we are lucky to have the opportunities this country affords, no matter how divided our country may feel at times.

A Chance to Serve

For us, one of the most important parts of our lives is joining you on your journey and serving you as you pursue your goals. It is truly our joy to celebrate with you when you reach a milestone and support you when life gets shaky.

There aren’t many people who can say they get to go to their dream job every day, so we are incredibly grateful that we get to do just that, providing education and support for so many families in our community who are on the road to a confident financial future.

As we reflect on all we’re grateful for this year, we want to make sure to thank you, our clients, for choosing Rosemeyer Management Group to guide you in your financial life. We look forward to investing in you and your family in the future!

Give Thanks

We truly hope your Thanksgiving leaves you refreshed and ready to look forward with anticipation. Please remember that through it all, we are here for you and your family—just a phone call away. Schedule an appointment online or by calling us at 608-348-2274. Feel free to reach out to me at carter@rosemeyermg.com with your questions, concerns, or just to touch base before the end of the year. We are thankful for you and your continued trust in RMG!

About Carter

Carter Klaas is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Carter focuses on the people behind the dollars and cents, forging long-lasting relationships with his clients. Using clear, measurable financial goals, Carter works to bring financial confidence to those he calls clients through education, intentional planning, and a strong relationship built on mutual trust. By planning comprehensively with investment strategies, risk management strategies, retirement planning, tax planning, and estate planning, Carter makes sure all the pieces of a person’s financial “puzzle” fit and work together for their goals. He is dedicated to personalized planning because he realizes that the wide-ranging experiences and emotions revolving around money demand a custom-fit plan. Carter has a bachelor’s degree in personal finance and financial planning from the University of Wisconsin-Madison.

When he’s not at work, Carter enjoys spending time with his wife, Natalie, and their Goldendoodle puppy, Willow. You’ll find them taking walks, drinking wine, bike rides, and being near the lake. To learn more about Carter, connect with him on LinkedIn.

Sure, nobody likes to pay taxes—and capital gains taxes are no exception. But think of it this way: you were smart (or lucky) enough to make the right investment decisions and now you get to cash in on the appreciation.

Although those gains will also come with a tax bill, fortunately, there are steps you can take to legally minimize your tax liability. Here are four tips to keep the IRS from taking a big bite out of your capital gains.

1. Wait a Little Longer to Sell

Timing the sale of your investments is critical to lowering your capital gains taxes. Selling your shares after holding for less than a year will result in a short-term capital gains tax. This means that all the gains you made from the sale of the stock will be taxed at your ordinary income rate, which can be 32%-37% for high-earners. Holding on to an asset for more than one year will be taxed at the long-term capital gains tax rate, which can be 0%, 15%, or 20%.

Holding periods are also critical when it comes to the sale of real estate. If you sell your primary home and you lived in the home for at least two years of the five-year period before the sale, the IRS allows you to exclude the first $250,000 of capital gains (or $500,000 for a married couple filing jointly). While the capital gains exclusions do not apply to investment properties, you may be able to utilize like-kind exchanges to defer capital gains tax by reinvesting in other real estate.

2. Utilize Tax-Loss Harvesting (TLH)

Losing money on your investments is usually a bad thing, but utilizing a tax-loss harvesting strategy means you can claim capital losses to offset your capital gains. If you show a net capital loss, you can use the loss to reduce your ordinary income by up to $3,000 (or $1,500 if you are married and filing separately). Losses above the IRS limit can be carried over to future years. Sometimes it is advantageous to sell depreciated assets for this reason. A tax-loss harvesting strategy can help minimize your tax liability and keep more money in your pocket. However, trying to reduce taxes shouldn’t come at the expense of maintaining a thoughtful asset allocation in your portfolio.

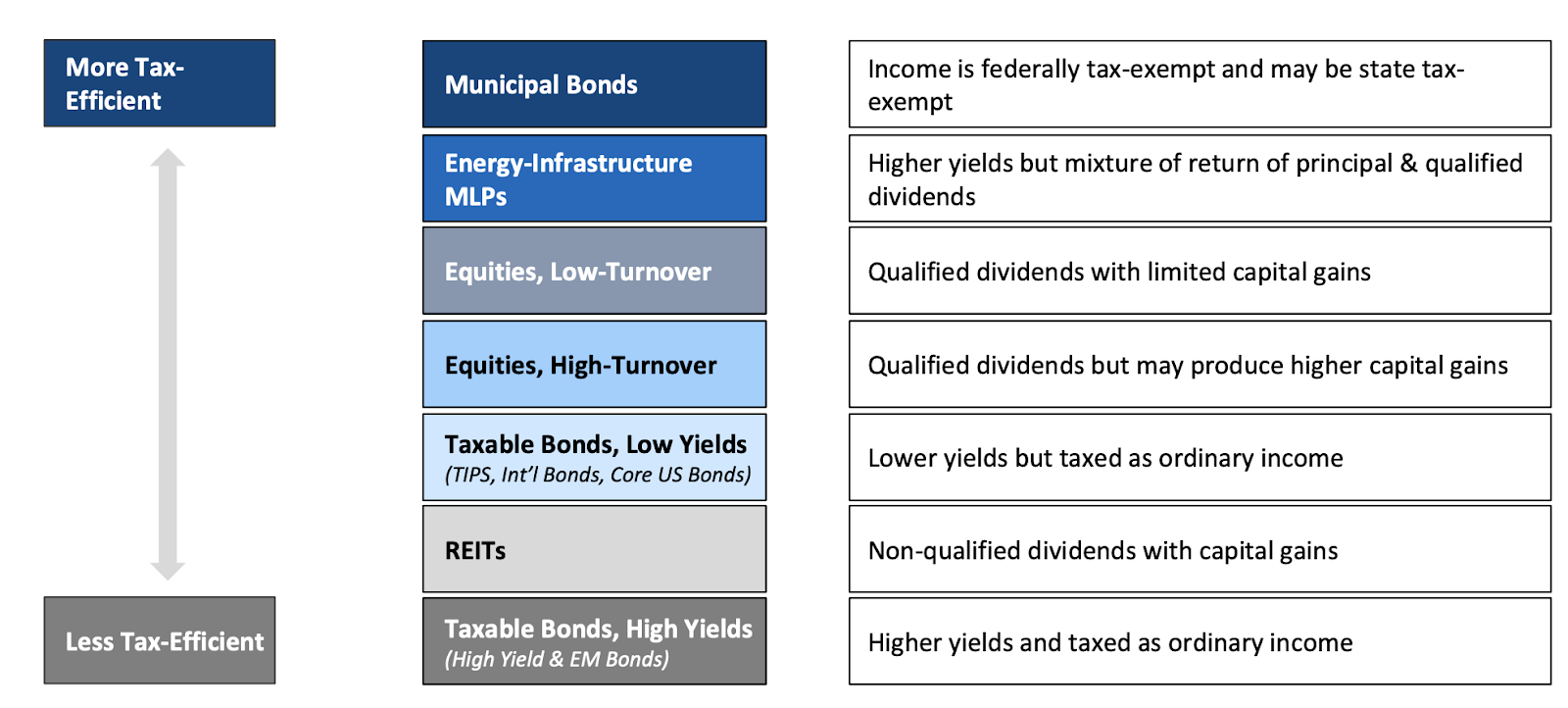

3. Consider Tax Efficiency of Funds Held in a Taxable Account

Some investments will be more tax-efficient than others, as illustrated by the chart below. For example, equities with low turnover will be more tax-efficient than equities with high turnover because there is less potential for capital gains. Active equities will translate into more capital gain income than passive equities, so holding an active investment in your taxable account could cost you tax dollars when you did not make a trade or take dollars out of the investment account. If you have noticed that you have large capital gain distributions and you didn’t sell anything in your taxable investment account, you likely have actively managed funds and it might make sense to look for passively managed funds to reduce your tax liability.

4. Understand Cost Basis & Share Lots

When you buy any amount of stock, the stock is assigned a lot number regardless of the number of shares. If you have made multiple purchases of the same stock, each purchase is assigned to a different lot number with a different cost basis (determined by the price at the time of each purchase). Consequently, each lot will have appreciated or depreciated in different amounts. Some brokerage accounts use first in, first out (FIFO) by default. If you utilize FIFO, your oldest lots will be sold first. Sometimes FIFO makes sense, but not always. Sometimes it is ideal to sell lots with the highest cost basis, which is commonly done as part of a tax-loss harvesting strategy.

Passing on assets as an inheritance can also increase your cost basis. Assets passed on to the next generation at the time of death allow your heirs to pay tax only on capital gains that occur after they inherit your property, through a one-time “step up in basis.” For example, when one spouse dies, assets passed on to the surviving spouse will have a cost basis of the price of the asset on the day in which they passed. This eliminates the deceased spouse’s portion of capital gains.

We’re Here to Help

There are many facets to your overall financial well-being; minimizing capital gains taxes is just one component. Keep in mind that having to pay capital gains taxes is a positive sign that your investment strategies are doing well. Partnering with a financial professional can help you create a holistic plan that is optimized to reach your financial goals.

At Rosemeyer Management Group, it’s our goal to help you build a customized road map for your finances so you can look forward to a comfortable retirement and decrease financial worry. Schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to reach out to me at kaley@rosemeyermg.com.

About Kaley

Kaley Bockhop is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Kaley’s experience in taxes and accounting and her financial planning expertise allows her to help her clients work toward their retirement goals and set themselves up for success. It is Kaley’s goal to partner with her clients to build a customized road map for their finances so they can look forward to a comfortable retirement and decrease financial worry. Kaley is a CPA and a CERTIFIED FINANCIAL PLANNER™ professional. She has a bachelor’s degree in science from the University of Wisconsin-Platteville with a triple major in accounting, agricultural business, and animal science, and a minor in biology. In her free time, Kaley enjoys working on her family’s farm where they raise nationally recognized registered Angus show cattle. She also loves exercising and traveling. To learn more about Kaley, connect with her on LinkedIn.

Who would have thought that retirement planning involved so much math? It can be easy to get lost in all the numbers: percentages, rates, yields, earnings, and returns. You might hear these words over and over but what about all the other factors involved in planning for retirement?

One of the variables that often gets overlooked is healthcare. This one aspect has the potential to make or break your retirement plan. If you aren’t prepared when a health difficulty arises, your finances could be seriously impacted. Here are some smart moves to make now to help avoid any potential risks to your ideal retirement.

What Health Costs Affect Retirees?

How big of a crisis could you be facing with health costs? According to Fidelity, the average retired couple faces upwards of $387,000 in health-related expenses. (1) And that is before calculating long-term healthcare costs, which can be some of the heftiest expenses of all!

In addition to being prepared for the inevitable health expenses that occur throughout retirement, there are a few insurance expenses that can catch you off guard if you aren’t aware of them.

For example, many people don’t realize they are not eligible for Medicare until age 65, regardless of what age they retire. If you lose your employer insurance by retiring at age 60, you will need to float marketplace or private insurance for 5 years, at a rate that will likely be 3-4 times more expensive.

The Benefits of an HSA

An HSA (or health savings account) is a great way to help mitigate some of these health expenses. An HSA is a tax-advantaged savings program, like a 401(k) or an IRA, sheltering your savings from taxes as long as they are used for health-related expenses.

The great thing is that an HSA can be invested freely into the same types of avenues as a 401(k), gaining compound interest to potentially build a considerable resource in the event of a medical crisis.

One way you can think of an HSA is as an investment account wrapped in a warm, fuzzy, tax-exempt blanket that will let your money go much further than if you had to pay taxes on it first.

Getting Your Medicare Coverage Right

One other area of retirement health that can be a bit tricky to get a handle on is the area of Medicare. Like most blessings that come down from the government, it is neither simple nor completely comprehensive.

Medicare Part A offers coverage for hospital bills that exceed your deductible. This coverage is for all qualifying 65+-year-olds. It is important to know that Part A has gaps in coverage. You will want to look into covering those gaps through secondary insurance called a Medigap policy.

Medicare Part B is optional coverage for medical expenses, and Part D is optional coverage for prescriptions. Both Part B and Part D require an additional premium that needs to be considered when planning for retirement expenses.

We’re Here to Help

It can be overwhelming to look at all the options for healthcare coverage in retirement. You may have lots of questions—and you may not even know which questions you need to ask. This is why it’s a wise decision to work with an experienced professional who can guide you through your options and provide specific, customized advice. Don’t procrastinate and put your future at risk!

At Rosemeyer Management Group, we focus on comprehensive wealth management to create a retirement plan that is unique to your goals and desires. Our advisors would love to sit down with you and walk through your retirement healthcare plan to determine if you are on track for your ideal retirement. Schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to email us at regan@rosemeyermg.com.

About Regan

Regan Shipp is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Regan is known for building relationships and looking at the whole picture of her clients’ lives to provide personalized, comprehensive wealth management services and advice. She leaves no stone unturned as she integrates investment strategies, risk management strategies, tax planning, retirement planning, and estate planning to design a plan that will help her clients pursue both financial success and freedom throughout their lives. Regan strives to educate her clients so they can feel empowered to take the actions necessary to achieve their goals. Regan is passionate about making a difference in people’s lives and loves journeying with her clients and seeing them reach new levels, surpass goals, and create wealth they might not have known was possible. Regan has a bachelor’s degree in accounting and agricultural business from the University of Wisconsin-Platteville and is a Certified Public Accountant (CPA) and CERTIFIED FINANCIAL PLANNER™ professional.

When she’s not at work, you can often find Regan spending time with her friends and family or out on a run training for a half or full marathon. Regan and her husband, Payton, and their dog, Axel, love the outdoors and look forward to more camping, deer hunting, and beach trips. To learn more about Regan, connect with her on LinkedIn.

________________

Parents have been there for you for decades. Knowing one day the roles will be reversed and you will be the one to look after them can be a difficult pill to swallow. You may already help them with little things like lifting heavy boxes or logging them into their Facebook account, but they’re also going to require lots of assistance with more important things like managing their finances and estate.

Stepping into a new caretaker role can get overwhelming, but having a plan in place can help ease the burden of responsibility, especially during a stressful time of transition. The following legal and financial considerations are important to keep in mind when planning for your aging parents’ financial legacy.

1. Get That Will in Place!

How many times have you heard a story in the news about a celebrity who died without a will and left their relatives and business partners with a raucous legal battle? Case in point: The battle over Jimi Hendrix’s estate continues to this day (more than 50 years later!) all because he had no will. (1)

While you may consider your family above such squabbles, it’s better not to test that assumption. You never know how large amounts of money will affect people and their behavior. Your parents need to have a will that spells out their final wishes, including who will carry out those wishes as the executor of their estate.

This is especially important in situations with blended families. It’s all too common for someone to neglect to update their will and leave an ex-wife or ex-husband as the sole inheritor or executor of an estate. Not only do your parents need a will, but they also need to make sure it is updated to reflect their current situation and desired legacy.

The importance of double-checking beneficiary designations goes beyond just a will. Make sure your parents have gone through all of their accounts, including life insurance policies, retirement accounts, and other savings, and verified that their listed beneficiaries are correct.

2. Start the Long-Term Care Conversation

If your parents are over 65, there’s a 70% chance they’ll need some sort of long-term care services in their lifetime. (2) That’s a high possibility that should be taken seriously.

Your whole family needs to come together to develop a plan for caring for your parents when the time comes. Discuss topics such as: Who will provide care for them? Who will pay for the care? Does it make sense for them to purchase long-term care insurance?

All too often, the most responsible or local son or daughter ends up shouldering the entire burden. This leads to burnout and resentment toward the other siblings. Save your family the trouble and proactively come up with a plan that everyone can agree on.

3. Assign Roles and Responsibilities

Approximately one in nine people age 65 and older are living with Alzheimer’s. (3) There’s a chance that a time will come when at least one of your parents is no longer able to make decisions for himself or herself. Who is going to make decisions for them at that point, both financial and medical?

While this can be an uncomfortable conversation, don’t avoid it. This is something you need to discuss with your parents and get the proper legal documents in place before they become incapacitated. Having simple powers of attorney written up will save you the trouble of going to court to request the right to help your parents when they need it most. And if your parents are comfortable with it, it would be a good idea to have one or more of their kids added to a bill-paying account. This way, if an emergency situation arises, they can access cash reserves to pay bills and debt payments immediately instead of waiting for assets to be released or legal documents to be enacted.

4. Invest in Your Relationship

While it is important to have all of the proper legal documents in place and have a plan for how to take care of your parents when they can no longer take care of themselves, for most people, their biggest regret is simply that they didn’t make the most of their time with their parents.

We all know that our time here on earth is limited, so we need to spend it investing in those we love. As you watch your parents age, it’s a visual reminder that your time with them is coming to an end. Consider creating a routine to make sure you spend time with them frequently while you still can. Can you make a standing date for breakfast on Fridays or a phone call on Sunday afternoons? Carving time out of your busy schedule for your parents is one of the very best ways to prepare for these final years of their lives.

5. Enlist the Help of a Professional

Attempting to manage your parents’ financial situation on your own can feel overwhelming with all the decisions to make and various family opinions to contend with. Parents may also not be receptive to these difficult conversations with their children and the role reversal they find themselves in. This is where the help of an experienced financial advisor can make a world of difference for everyone involved. Someone knowledgeable and skilled in helping families make important decisions about such things as wills, retirement, and estate planning can be a great asset in these sensitive situations.

At Rosemeyer Management Group, we are dedicated to supporting, educating, and providing informed direction to every client. If you would like help planning for your parents’ future, schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to reach out to me at payton@rosemeyermg.com.

About Payton

Payton Simon is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Payton spends his days providing in-depth investment analysis and aiding in the development of customized, comprehensive retirement, tax, and estate planning strategies to help his clients reach their retirement goals. Payton is passionate about doing his best for every client he serves and making sure they don’t have any blind spots or missed opportunities in their financial plan. He strives to do his part to close the financial literacy gap so people can feel confident and empowered about their financial future. Payton has a bachelor’s degree in finance with a minor in accounting from the University of Wisconsin-LaCrosse. Outside of work, Payton is active in his local Catholic parish and incorporates his faith into every aspect of his life. He loves spending time with his family and friends and is a sports enthusiast, playing golf, basketball, and baseball. To learn more about Payton, connect with him on LinkedIn.

_______________

(1) https://www.guitarplayer.com/news/the-estates-of-jimi-hendrix-and-noel-redding-and-mitch-mitchell-are-suing-each-other-heres-whats-going-on#:~:text=The%20estates%20of%20all%20three,from%20streaming%20and%20digital%20media.

(2) https://acl.gov/ltc/basic-needs/how-much-care-will-you-need

(3) https://www.alz.org/alzheimers-dementia/facts-figures

With the news full of economic woes these days, from interest rate hikes to sliding stock market indices, it can feel like our world is spinning out of control. In stressful economic times, it can be tempting to panic, especially when it comes to our finances. We are, after all, naturally averse to loss, and the pain of losing is more powerful than the potential to achieve gains. (1)

Here’s the caveat: when we make emotional decisions, we sometimes act irrationally in an attempt to avoid loss, causing us to lose even more. Just ask any investor who has sold stock when the market dropped and missed the recovery, only buying back in when the markets were high again.

You know you need to invest to grow your money into a nest egg that will sustain you in the future, but what can you do to prevent taking on too much risk in the process?

What Does Risk Tolerance Really Mean?

In the financial world, risk tolerance is defined as a measure of one’s financial ability to withstand losses. While you can’t completely eliminate risk in your portfolio, you can ensure that the amount of risk you take correlates with the level of potential reward for you to gain. It is more than possible to match your investments to your goals while still being able to sleep at night during market downturns.

Here’s the thing we need to remember when we’re tempted to get out of the market ASAP: some risks are avoidable, some are not. Avoidable risks are those that occur when your portfolio leans too heavily on stocks or bonds that have been unstable in the past or when your holdings are not diversified appropriately. For example, you may be putting too much of your company’s stock in your 401(k) plan. Or you may have an overabundance of overlapping U.S. stock mutual funds instead of being more globally diversified. Avoidable risks often occur when we underestimate risk and believe we can tolerate more than we actually can.

On the other hand, unavoidable risks are those that occur because our world is ever-changing, volatile, and we can’t predict everything. As much as we wish they weren’t, unavoidable risks are simply out of our control. This type of risk includes unfortunate events like geopolitical issues, global pandemics, and economic recessions.

The third category of risk is often unseen, but it can impact your portfolio just as intensely as an obvious risk: the risk of being too conservative and not achieving your future goals as a result. By overestimating risk and trying to avoid loss at any cost, you could be unintentionally sacrificing your future dreams.

How Can I Be Comfortable With Risk?

Wouldn’t it be nice if you could just tell your advisor you’re comfortable taking on “moderate” risk? The truth is that everyone, based on their age, life circumstances, personality, and time horizon, has their own unique risk tolerance level. How do you pinpoint how much risk you are comfortable taking, how much risk you need to take to reach your goals, and how much risk you currently have in your portfolio?

That’s where an experienced financial advisor comes in and can make a world of difference. At Rosemeyer Management Group, we are dedicated to providing retirement plan investment management and strategic planning. Simply put, we strive to be our clients’ trusted advisor. As a financial advisory firm, our focus is to provide unbiased opinions for the purpose of long-term investment results, increased employee satisfaction, and reduced employer liability—all while keeping plan costs transparent. Schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to reach out to me at carter@rosemeyermg.com.

About Carter

Carter Klaas is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Carter focuses on the people behind the dollars and cents, forging long-lasting relationships with his clients. Using clear, measurable financial goals, Carter works to bring financial confidence to those he calls clients through education, intentional planning, and a strong relationship built on mutual trust. By planning comprehensively with investment strategies, risk management strategies, retirement planning, tax planning, and estate planning, Carter makes sure all the pieces of a person’s financial “puzzle” fit and work together for their goals. He is dedicated to personalized planning because he realizes that the wide-ranging experiences and emotions revolving around money demand a custom-fit plan. Carter has a bachelor’s degree in personal finance and financial planning from the University of Wisconsin-Madison.

When he’s not at work, Carter enjoys spending time with his wife, Natalie, and their goldendoodle puppy, Willow. You’ll find them taking walks, drinking wine, watching the sun set, and being near the lake. To learn more about Carter, connect with him on LinkedIn.

_____________

My clients always ask me how I manage my own money as if it’s a secret that I keep to myself. The thing about money management is that people often feel like no matter how much they learn about the latest techniques and trends, they’re never quite doing it right, that there’s always some better way to save or to invest.

Well, as a Certified Public Accountant (CPA) and CERTIFIED FINANCIAL PLANNER™ professional who works with wealth management strategies every day, I’m here to tell you that the way I manage my own money is not all that different from how I manage my clients’ money. Here are the three things I focus on the most when investing my own money.

Active vs. Passive Investing

One of the most important aspects of my personal investment plan is the distinction between active and passive investing. At Rosemeyer Management Group, we focus on passive investing because it has generally outperformed active management over the long term. However, there is no guarantee one strategy will outperform the other. (1)

Passive investing utilizes strategies like buy-and-hold or indexing, while active investing involves single-stock investing and frequent buying and selling in an attempt to beat the average returns of the market. As expected, active management comes with added expenses and no guarantees that the returns will be any better than a passively invested portfolio. In fact, active investing often results in worse returns when the increased costs are factored in. (2)

Trying to pick and choose individual stocks has proven to be a losing game many times

and something we encourage clients to avoid. But single stocks are not the only investing strategy that’s actively managed. Many mutual funds also utilize this strategy, and clients might not even realize that they are overpaying for these services when they could achieve the same allocation through a low-cost index fund. Checking out a mutual fund’s turnover rate on Morningstar is a great way to ensure you know how it’s invested and managed.

Diversification

Next, diversification is a critical piece of any investment plan. It can be achieved through an asset allocation strategy that considers which components of your plan can move together and which can act as a hedge against downside risk. Diversification can’t guarantee a minimum level of return, but it will at least act as a buffer against the inherent volatility of the market. By investing across and within several different asset classes, you can reduce your overall exposure to risk.

While it can be tempting to chase performance and overload a portfolio with the hottest asset class, I prefer to take a more balanced (and diversified) approach when investing my own money. This mindset aligns with how we manage our clients’ funds at Rosemeyer Management Group. Our portfolio options include diversified allocations in:

- Large-cap growth

- Large-cap value

- Mid-cap

- Small-cap

- Diversified international

- Emerging market

- Fixed income

This provides broad exposure to several different industries, sectors, and asset classes across the market, with the strategy that no single investment can drastically alter the returns of the whole portfolio. If a client comes to us with their own allocation, we feel they should be able to tell us exactly why they are invested that way. Oftentimes clients don’t realize how much unnecessary risk they take on by not properly diversifying their portfolios.

Not All Bonds Are Created Equal

Similarly, clients often don’t realize that traditional “safe” investments like bonds no longer provide the guarantees they used to 40 years ago. In 1982, you could achieve an average yield of 13.01% with a relatively low-risk investment in long-term bonds, but that is no longer the case. (3) As of June 7, 2022, the yield on a 10-year bond is only about 3.31%! (4)

Given the interest-rate environment we find ourselves in, not all bonds are created equal. The Federal Reserve has already raised interest rates twice and they are very likely to continue raising rates throughout the rest of 2022. (5) Because of this, we believe that short-term bond funds are a much better choice for the fixed income portion of an investment portfolio as opposed to longer-term bonds.

This is because interest rates are inversely related to bond prices, and the longer the bond’s maturity, the more intense this relationship is. So longer-term bonds will likely lose their value much more quickly and intensely as interest rates continue to rise. Paying attention to the duration of a fixed-income investment has never been more important than it is in today’s investment environment.

How We Can Help

Successful money management and investing don’t have to be shrouded in mystery. At Rosemeyer Management Group, our goal is to give our clients the tools and resources they need to feel confident in their financial plans. If you’d like to learn more about our investment philosophy and how it applies to your portfolio, schedule an introductory appointment online or by calling us at 608-348-2274.

Disclosure: Bond prices can fluctuate, like the value of any other investment. Past performance doesn’t guarantee future results.

About Regan

Regan Shipp is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Regan is known for building relationships and looking at the whole picture of her clients’ lives to provide personalized, comprehensive wealth management services and advice. She leaves no stone unturned as she integrates investment strategies, risk management strategies, tax planning, retirement planning, and estate planning to design a plan that will help her clients pursue both financial success and freedom throughout their lives. Regan strives to educate her clients so they can feel empowered to take the actions necessary to achieve their goals. Regan is passionate about making a difference in people’s lives and loves journeying with her clients and seeing them reach new levels, surpass goals, and create wealth they might not have known was possible. Regan has a bachelor’s degree in accounting and agricultural business from the University of Wisconsin-Platteville and is a Certified Public Accountant (CPA) and CERTIFIED FINANCIAL PLANNER™ professional.

When she’s not at work, you can often find Regan spending time with her friends and family or out on a run training for a half or full marathon. Regan and her husband, Payton, son, Lincoln, and their dog, Axel, love the outdoors and look forward to more camping, deer hunting, and beach trips. To learn more about Regan, connect with her on LinkedIn.

_______________

(1) https://www.forbes.com/advisor/investing/passive-investing-vs-active-investing/

(2) https://www.forbes.com/advisor/investing/passive-investing-vs-active-investing/

(3) https://www.macrotrends.net/2016/10-year-treasury-bond-rate-yield-chart

(4) https://www.macrotrends.net/2016/10-year-treasury-bond-rate-yield-chart

(5) https://www.bankrate.com/banking/federal-reserve/how-much-will-fed-raise-rates-in-2022/

Some things in life captivate us from a young age and never stop fascinating us. For me, that something is finance. This fascination began with an unfortunate event: the housing market crash and subsequent Great Recession of 2008. But often in life, good things can come out of difficult times, and that’s what happened for me.

While the Great Recession had a global impact, it also became very personal as I felt the financial burden this crisis placed on my parents and family. This led me to begin researching and learning about the inner workings of financial markets, and not long after, I was hooked! This new interest and growing knowledge, combined with my innate gift for numbers, has led me to the path I am on today as a financial advisor.

Finding My Way

This path was not always clear to me. I’ve always had a knack for numbers, but could never visualize a meaningful career utilizing that skill set. Even after discovering my passion for finances, I did not necessarily imagine my future career in financial services. Still, I knew this was the direction I wanted to follow, so I pursued a degree in finance with a minor in accounting from the University of Wisconsin-La Crosse. Prior to and throughout college, I held various jobs that grew and added to my skill set, working as a farm hand during the summers, then in the restaurant industry. These experiences helped develop my work ethic, communication, and people skills, which are all valuable assets in my current position.

Though my skills in math and my passion for the financial industry work very well together, I didn’t make the connection to utilizing those in a career as a financial advisor until I had the opportunity to work for the Rosemeyer Management Group four years ago. During my internship as a research analyst, I quickly realized that I was meant to be a financial advisor. I was able to combine my math skills and knowledge of financial markets, but, more importantly I was given the opportunity to serve families and individuals—which I now realize is my true calling in life. Being able to serve others intentionally in the setting of the RMG family has been such a blessing and gives me the assurance that being a financial advisor is the perfect career for me. Very rarely do people’s passions, skills, and abilities line up with their career, but I am lucky enough to do what I love every day.

On the Right Path

Once the lightbulb went off and I realized that a career as a financial advisor was the perfect culmination of my education, skills, and passions, I gained momentum toward pursuing this goal. In 2021, I graduated with my degree and became an investment advisor representative with Rosemeyer Management Group. My days here are spent working hard to create comprehensive and customized financial plans for our clients so they can reach their retirement goals. I aim to educate and empower clients, helping them understand how to make their hard-earned money work hard for them.

I am passionate about serving our clients because in each one of them I see my parents, or my siblings, or any of my loved ones. I see people who work hard for their families and themselves. I am honored that my clients allow me to assist them on their financial journey to make sure their hard work pays off in the form of sound financial decisions. I am also passionate because I believe that for many years this industry did not have the best interests of the average American at heart. My hope is to help redefine the financial industry as one that helps the blue-collar family rather than harms it.

A Fulfilling Journey

One of the most fulfilling parts of my job is working alongside clients, helping them through their financial difficulties and celebrating their successes. Seeing clients realize they have achieved their long-desired financial and personal goals never gets old. This joy and respect for the hard work of our clients is what drives me to serve them humbly and honestly every day. I am also honored to work for this firm and with coworkers who are like family.

When we start out on a journey, the path may not always be clear, and we may not even know where we are headed; but if we have faith and follow God’s will for us, pursuing the next right step, we will end up right where we’re supposed to be. That’s where I find myself today and I’m so grateful to be here.

Take the Next Step

Here at Rosemeyer Management Group, we’re always open to meeting new people and seeing how we may be able to help. Whether you’ve already started planning for the future or have yet to put strategies in place, we encourage you to reach out today for a no-obligation conversation to see if we’d be a good fit. Schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to email us directly at payton@rosemeyermg.com.

About Payton

Payton Simon is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Payton spends his days providing in-depth investment analysis and aiding in the development of customized, comprehensive retirement, tax, and estate planning strategies to help his clients reach their retirement goals. Payton is passionate about doing his best for every client he serves and making sure they don’t have any blind spots or missed opportunities in their financial plan. He strives to do his part to close the financial literacy gap so people can feel confident and empowered about their financial future. Payton has a bachelor’s degree in finance with a minor in accounting from the University of Wisconsin-LaCrosse. Outside of work, Payton is active in his local Catholic parish and incorporates his faith into every aspect of his life. He loves spending time with his family and friends and is a sports enthusiast, playing golf, basketball, and baseball. To learn more about Payton, connect with him on LinkedIn.

Financial planning isn’t just about the numbers, it’s about your life. But it can be difficult to know where to start and how to create a plan that reflects your values, personality, goals, and circumstances.

We at Rosemeyer Management Group understand how difficult it can be to find the time or energy to devote to necessary but overwhelming tasks, such as investing and financial planning. Our priority is to help you manage your finances and take action to achieve your financial goals.

Who We Are

Jim Rosemeyer founded Rosemeyer Management Group in 2010. After dealing with several financial advisors throughout the course of his chiropractic career, it became clear to Jim that there was a strong need for comprehensive wealth management that was both effective and easy to understand. His mission became educating and working with individuals and retirement plans to better help them realize their retirement goals and dreams.

Rosemeyer Management Group is an SEC Registered Investment Advisor specializing in Comprehensive Wealth Management by focusing on retirement planning, investments, tax planning, estate planning, and life insurance.

We are dedicated to providing comprehensive wealth management and strategic planning to high-net-worth individuals and employer-sponsored retirement plans. Simply put, we strive to be our clients’ trusted advisor in all things financial.

What We Do

We offer comprehensive financial planning to individuals and families. This includes:

- Retirement planning

- Investment advice

- Income withdrawal strategies

- Health insurance transitions

- Strategic tax planning

- Estate planning

- Insurance analysis

- Social Security planning

We also provide investment advice and strategic planning to many retirement plan providers. We specialize in 401(k), 403(b), SEP, and SIMPLE plans and can help you achieve long-term investment results and increased employee satisfaction.

Who We Serve

We serve a wide range of clients, but typically specialize in helping people between the ages of 59½ – 65 who are preparing to retire. Many of our clients come to us unsure if they are in a position to retire comfortably. They may not know if their money will carry them throughout the remainder of their lifetime, and they are overwhelmed with all the decision-making that comes along with retirement.

We will walk you through the pre-retirement challenges you face and ensure you are in a position to retire with confidence.

Our clients are everyday hardworking individuals who want to live out the American dream. They are humble enough to ask for help and truly care about planning for themselves and their families, no matter their circumstances. They ask important questions and see themselves as collaborators, willing to build their own versions of success—it’s our job, financially speaking, to help them do that.

Why Clients Choose Us

Clients choose us because of our open, honest, and collaborative approach to planning. Our clients know we do far more than invest their portfolios; we provide comfort and guidance on all aspects of their financial life.

The level of service at Rosemeyer Management Group is unparalleled. Rather than treating clients like another number walking through the door, we consider them a teammate in the financial planning process. Through our financial expertise, education, and transparency, our clients leave each meeting having learned something they can take to better their understanding of our recommendations and improve their financial situation.

We have a team of advisors always ready and willing to answer client questions and talk through concerns. We strive to build long-lasting relationships that leave our clients feeling valued and informed.

Get Started Today

At Rosemeyer Management Group, we understand the importance of comprehensive financial advice. Don’t settle for less than a full understanding of your financial picture. To learn more about our process and how we can help you, schedule an introductory appointment online or by calling us at 608-348-2274. For any questions, feel free to reach out to me at kaley@rosemeyermg.com.

About Kaley

Kaley Bockhop is an investment advisor representative at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. Kaley’s experience in taxes and accounting and her financial planning expertise allows her to help her clients work toward their retirement goals and set themselves up for success. It is Kaley’s goal to partner with her clients to build a customized road map for their finances so they can look forward to a comfortable retirement and decrease financial worry. Kaley is a CPA and a CERTIFIED FINANCIAL PLANNER™ professional. She has a bachelor’s degree in science from the University of Wisconsin-Platteville with a triple major in accounting, agricultural business, and animal science, and a minor in biology. In her free time, Kaley enjoys working on her family’s farm where they raise nationally recognized registered Angus show cattle. She also loves exercising and traveling. To learn more about Kaley, connect with her on LinkedIn.

What many experts once thought to be “transitory” inflation has stuck around a lot longer than expected, with no signs of stopping. The January CPI inflation report shows that consumers are continuing to struggle through some of the highest inflation in decades. Prices in January 2022 increased 0.6%, which is higher than the increase of 0.5% we saw in December 2021. (1)

Watching your purchasing power fall faster than expected can be a frightening thing, but the best way to assess the situation is to take a look at the factors surrounding why inflation is rising. The COVID-19 pandemic was unlike anything the world has ever seen; the rebound from such an event will be just as much of a learning curve.

High inflation rates don’t necessarily mean we are going to be the next Zimbabwe or Venezuela. It just means we need to plan for the future and mitigate potential risk. Here are some reasons why inflation has increased in the past year and what it means for your long-term purchasing power.

What Is Inflation?

According to Investopedia, inflation is a decrease in the purchasing power of money, reflected in a general increase in the prices of goods and services in an economy. (2) It can be characterized as persistent or transitory. Transitory inflation (3) is temporary and happens when supply doesn’t meet demand. If left unhandled, it can turn into persistent inflation, (4) which results in a more permanent increase in prices due to a continuous mismatch in supply and demand.

The Consumer Price Index (CPI) is a common measure of inflation. The most recent CPI report from January 2022 suggested that inflation has risen an astounding 7.5% over the past year! (5) That is significantly higher than the typical 2% rise we see in an average year.

Why Is Inflation So High?

To better understand if inflation will last, let’s take a look at the factors contributing to its rise.

Devalued Dollar

When the COVID-19 pandemic first hit and millions of Americans were furloughed or laid off, drastic economic measures were taken to keep the country afloat. The U.S. government instituted expansionary monetary and fiscal policies in order to pump money back into the economy, increasing the money supply at a rapid rate. It jumped from $15.5 trillion in February 2020 to $18.8 trillion in October 2020, an increase of over $3 trillion. (6)

Though experts agree that these drastic measures were necessary to keep the economy from collapsing, they also agree that the increase in money supply devalued the dollar, meaning it takes more dollars to buy the same item since each dollar is less valuable.

This issue is further compounded by the current trade deficit, which is sitting at a $182.4 billion (27%) year-to-date increase. (7) Because the U.S. buys (imports) more than it sells (exports), a devalued dollar relative to other countries’ currencies drives the cost of imported goods up even more. It’s tempting to write these issues off as fallout from the pandemic, but the trade deficit is not a new issue. In fact, the U.S. has seen a deficit every year since 1975. (8) This indicates that the rise of inflation is not a new issue either, it’s just been sped up and exacerbated by the increase in government spending in response to the pandemic.

Supply Chain Headaches

If there’s one thing that’s been in the news even more than inflation concerns, it’s supply chain disruptions. Since the vaccine rollouts and slow return to pre-pandemic life, companies have struggled to keep up with manufacturing and distributing goods. This is because many distribution centers cut their hours when the global economy came to a halt in anticipation of a huge drop in demand for consumer goods. The drop in demand, however, did not come.

As people across the globe spent days, then weeks, then months in their houses, demand skyrocketed for exercise equipment, home goods, and office supplies. Factories increased their output, but the distribution chains have struggled to get everything where they need to be.

Additionally, the increased production has also caused a shortage in raw materials, thereby exacerbating the gap between overall supply and demand for even basic items. As demand continues to outpace supply, prices are driven higher and higher.

Labor Shortages and Increasing Wages

Continued labor shortages are another factor driving inflation. In what is being called “The Great Resignation,” millions of workers across America have quit or considered quitting their jobs as they reevaluate the role that work plays in their lives. (9) As such, many companies are finding that they have to pay higher wages in order to attract and retain employees. These increased costs often get passed through to the customer in the form of increased prices for goods and services.

The flip side of the labor shortage issue is the passage of the $15 federal minimum wage. (10) Many states are following suit with plans to increase their respective minimum wage thresholds. So even if companies weren’t paying more for labor because of the struggle to find workers, they would still be paying more due to increasing minimum wage. Again, these increased costs will be passed through to consumers, and it will be more than just a transitory change in prices since the minimum wage laws are permanent.

How Long Will Inflation Last?

It’s tough to say exactly how long inflation will last, but based on these three variables, it could be a couple years before we return to the target rate of 2%. As our global economy shifts, trade alliances change, we experience the ongoing effects of the COVID-19 pandemic, it seems to be an issue that will persist for the foreseeable future.

Let Us Help You Protect Against Inflation

It’s understandable to be concerned about inflation. Many of us are not only worried about how inflation will impact our current finances, but also about how it will affect our long-term goals. That’s why it’s so crucial to be realistic about how long inflation could impact your financial plan.

At Rosemeyer Management Group, we have the tools and expertise to guide you through a long-term inflationary environment. We will review your investment and retirement plans for proper diversification and risk tolerance levels, ensuring you’re properly protected no matter how long this increased inflation lasts. Schedule an introductory appointment online or call us at 608-348-2274. For any questions, feel free to reach out to me at andrew@rosemeyermg.com.

About Andrew

Andrew Tranel is co-owner and chief investment officer at Rosemeyer Management Group, an SEC Registered Investment Advisor based in Platteville, WI. With 10 years of experience, Andrew specializes in providing retirement planning, tax planning, estate planning, and insurance needs for his retiree and pre-retiree clients with the goal of helping them develop a road map to financial freedom. He is known for his expertise in helping people make empowered and educated decisions about their retirement so they can confidently navigate the pre-retirement challenges they face. Andrew has a bachelor’s degree in finance and sport management from Loras College and is a CERTIFIED FINANCIAL PLANNER™ professional. When he’s not working, you can find Andrew spending time with his wife, Kimberlee, their three sons, Steven, Elliott, and Weston, and their beloved boxer, Bella. He also enjoys hunting, golfing, playing basketball and softball, and traveling. To learn more about Andrew, connect with him on LinkedIn.

_______________

(1) https://www.forbes.com/advisor/personal-finance/inflation-more-expensive-january

(2) https://www.investopedia.com/terms/i/inflation.asp

(3) https://finance.yahoo.com/news/inflation-transitory-persistent-210149448.html

(4) https://finance.yahoo.com/news/inflation-transitory-persistent-210149448.html

(5) https://www.bls.gov/news.release/pdf/cpi.pdf

(6) https://www.statista.com/statistics/1121054/monthly-m2-money-stock-usa/

(7) https://www.census.gov/foreign-trade/Press-Release/current_press_release/ft900.pdf

(8) https://www.thoughtco.com/history-of-the-us-balance-of-trade-1147456

(9) https://www.abc.net.au/news/2021-09-24/the-great-resignation-post-pandemic-work-life-balance/100478866

(10) https://www.dol.gov/newsroom/releases/whd/whd20210721